The 2026 compliance mandate for DeFi

By 2026, the regulatory landscape for decentralized finance has shifted from voluntary adoption to mandatory enforcement. Protocols that previously operated under the guise of non-custodial anonymity now face explicit legal requirements to implement robust identity verification systems. This transition is driven by a convergence of international regulatory frameworks and the increasing sophistication of AI-driven compliance tools.

In the European Union, the Markets in Crypto-Assets (MiCA) regulation has established clear guidelines for service providers, requiring comprehensive Know Your Customer (KYC) procedures. Similarly, in the United States, executive orders and FinCEN guidance have clarified that decentralized protocols facilitating fiat on-ramps or offering significant financial utility must adhere to anti-money laundering (AML) standards. These jurisdictions are no longer debating whether identity verification is necessary; they are enforcing it.

The integration of AI into KYC workflows is not merely a technological upgrade but a regulatory necessity. As noted by Moody's, AI can enhance KYC by analyzing vast amounts of data to detect suspicious connections and assign risk scores, allowing protocols to meet stringent regulatory demands efficiently. Without such automation, the cost and complexity of manual compliance would likely render many DeFi protocols non-viable in regulated markets.

Protocols should consider that the 2026 reality favors "bounded autonomy"—a controlled stack of automation and analytics that preserves human accountability at high-risk points. This approach aligns with regulatory expectations for transparency and oversight, ensuring that DeFi platforms can operate legally while maintaining the core principles of decentralization. The shift is not about eliminating privacy but about embedding compliance into the fabric of decentralized systems.

On-chain identity verification methods

AI-driven KYC systems in decentralized finance operate by merging traditional identity proofs with real-time blockchain analytics. This hybrid approach allows protocols to verify the legitimacy of a counterparty while simultaneously assessing their historical on-chain behavior. According to TCS, such systems rely on artificial intelligence, machine vision, and learning algorithms to simplify identity verification and automate risk profiling [[src-serp-6]].

The verification process typically follows three core stages: confirming the party’s legitimacy, creating a dynamic risk profile, and screening the subject against that profile [[src-serp-6]]. AI enhances this workflow by automating data analysis and significantly reducing false positives, which streamlines customer onboarding [[src-serp-2]]. Appian notes that sophisticated algorithms help differentiate between legitimate activities and fraudulent patterns more accurately than static rule sets [[src-serp-3]].

| Verification Stage | Traditional KYC | AI-Driven KYC |

|---|---|---|

| Data Input | Static documents (ID, passport) | Dynamic on-chain history + ID |

| Analysis Method | Manual review, rule-based checks | Automated extraction, ML risk scoring |

| False Positive Rate | Higher, due to rigid thresholds | Lower, via nuanced pattern recognition |

| Update Frequency | Periodic or event-driven | Continuous, real-time monitoring |

Protocols should consider that this shift requires robust data infrastructure. The integration of AI does not replace human oversight but rather prioritizes high-risk cases for manual review. This ensures that accountability remains with compliance officers while automation handles the volume of routine checks.

Self-sovereign identity and privacy limits

The tension between DeFi’s decentralized ethos and the demands of AI-driven KYC centers on data sovereignty. Traditional compliance models require users to surrender personal identifiers to centralized intermediaries, a practice that contradicts the pseudonymous nature of blockchain transactions. Self-sovereign identity (SSI) frameworks attempt to resolve this by allowing users to control their own credentials, but integrating these with AI verification systems introduces new privacy constraints.

Zero-knowledge proofs (ZKPs) have emerged as a technical bridge in this space. They enable protocols to verify that a user meets specific KYC criteria—such as age or residency—without revealing the underlying personal data. This approach aligns with the principle of data minimization, ensuring that only the necessary proof is transmitted. However, the implementation of ZKPs within AI-driven compliance stacks remains complex, requiring significant computational resources and standardized cryptographic protocols.

Regulatory bodies are increasingly scrutinizing the balance between privacy and transparency. The European Union’s Markets in Crypto-Assets (MiCA) regulation, effective in 2024, mandates strict AML compliance for crypto service providers, pushing the industry toward more robust identity verification methods. Similarly, the Financial Action Task Force (FATF) has updated its guidance to include virtual assets, emphasizing that privacy-enhancing technologies must not obscure illicit activities. Protocols should consider these regulatory trends when designing identity layers, ensuring that privacy features do not inadvertently facilitate non-compliance.

McKinsey & Company notes in a 2023 report that agentic AI is reshaping banking compliance by automating end-to-end KYC processes. This automation allows for real-time monitoring and dynamic risk profiling, which can reduce false positives and improve customer experience. However, the reliance on AI introduces risks related to algorithmic bias and data accuracy. Protocols should implement rigorous audit trails and human oversight mechanisms to mitigate these risks, particularly in high-stakes transactions.

The integration of SSI and ZKPs into DeFi protocols is not merely a technical upgrade but a strategic necessity for long-term viability. As regulatory frameworks evolve, the ability to provide verifiable, privacy-preserving identity solutions will become a key differentiator for DeFi platforms. Failure to address these privacy limits could result in exclusion from mainstream financial systems and increased regulatory scrutiny.

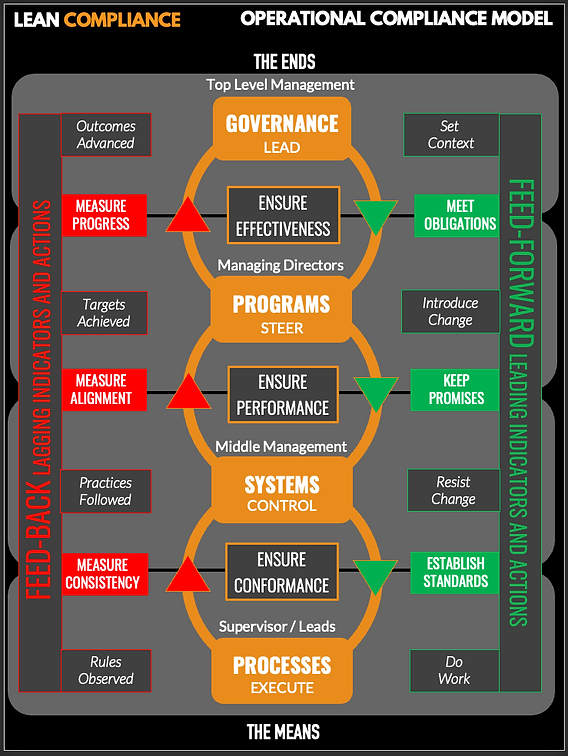

Bounded autonomy in compliance workflows

The prevailing narrative that artificial intelligence will fully automate Know Your Customer (KYC) processes is misleading. The 2026 reality for decentralized finance (DeFi) and traditional banking alike is not self-governing compliance, but bounded autonomy. This model positions AI as a controlled stack of automation, analytics, and assistive tools rather than a replacement for human judgment.

As noted in recent industry analysis, the most credible form of AI in KYC and AML is one that reduces manual effort and improves prioritization while preserving human accountability at the highest-risk points [src-serp-8]. Protocols should consider this distinction critical: AI excels at data extraction, document validation, and initial risk profiling, but it lacks the contextual nuance required for final adjudication in complex scenarios.

The Human-in-the-Loop Imperative

In high-stakes DeFi transactions, the margin for error is nonexistent. AI systems can flag anomalies with high speed, but they cannot interpret the intent behind suspicious behavior or interpret the gray areas of evolving regulatory guidance. Therefore, human operators must remain the final authority on high-risk decisions.

This approach aligns with the efficiency gains highlighted by firms like Capgemini, which emphasize that AI-driven automation streamlines processes by handling routine verification tasks, thereby allowing compliance teams to focus on complex, high-value cases [src-serp-5]. By offloading repetitive checks to AI, human reviewers can dedicate their expertise to nuanced risk assessments, ensuring that accountability remains firmly with the protocol’s compliance officers.

Preserving Accountability

Regulatory bodies increasingly expect clear lines of responsibility. If an AI system misclassifies a high-risk entity, the protocol is still liable. Bounded autonomy ensures that every automated decision is traceable and reviewable by a human expert. This structure not only mitigates legal risk but also builds trust with regulators who demand transparency in how identity and risk are managed.

Ultimately, the goal is not to remove humans from the loop, but to optimize their role. AI handles the volume; humans handle the verdict. This division of labor ensures that DeFi protocols can scale their compliance efforts without sacrificing the rigorous oversight required by global standards.

Checklist for DeFi protocol integration

Protocol developers should align their AI-driven KYC systems with 2026 compliance standards to ensure regulatory resilience. As noted by Moody’s, generative AI can enhance workflows by analyzing vast datasets to detect suspicious connections and assign risk scores, but it requires careful implementation to avoid false positives [1]. The 2026 reality favors bounded autonomy, where AI acts as a controlled stack of automation that reduces manual effort while preserving human accountability at high-risk points [2]. Protocols should consider the following steps to integrate these systems effectively.

Ensure all AI models are trained on verified, up-to-date data sources. Protocols should consider implementing real-time verification checks against official sanction lists and adverse media databases to maintain accuracy.

Set clear risk thresholds for automated decisions. AI should assign risk scores based on comprehensive profiles, but protocols should consider establishing manual review triggers for scores exceeding defined limits to mitigate false positives.

Maintain human oversight for high-risk decisions. While AI can streamline verification, protocols should consider retaining human reviewers for complex cases to ensure accountability and compliance with evolving regulatory expectations in 2026.

[1] Moody's, "Generative AI in KYC workflows" (2025) [2] KYC Chain, "AI Compliance Agents KYC AML" (2026)

No comments yet. Be the first to share your thoughts!