Why onchain KYC 2026 matters now

The regulatory landscape for tokenized assets is shifting from voluntary adoption to mandatory infrastructure. By 2026, the friction of traditional off-chain Know Your Customer (KYC) processes is no longer compatible with the velocity of on-chain settlement. Regulators are demanding that identity verification be embedded directly into the asset’s lifecycle, moving beyond static database checks to continuous, real-time compliance.

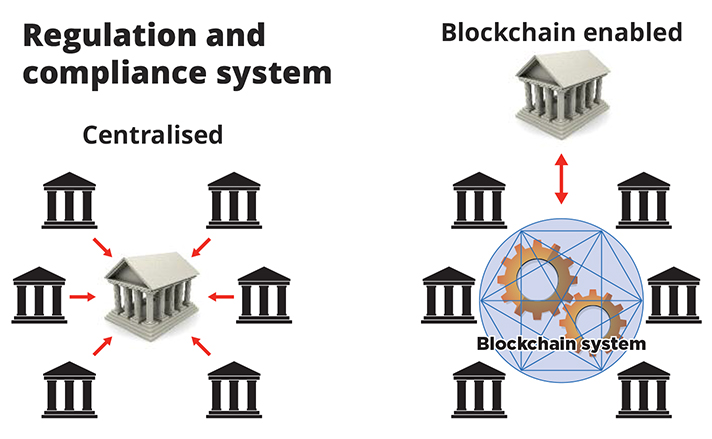

Traditional off-chain KYC creates a disconnect between the legal identity of an investor and the on-chain representation of their holdings. This gap allows for compliance decay, where an investor’s status changes—such as a sanction listing or expiring accreditation—without the token issuer being immediately notified. In contrast, onchain KYC 2026 integrates verification data directly into smart contracts via decentralized identity protocols and oracles. This ensures that every transfer is validated against current regulatory requirements at the moment of execution.

The shift from periodic off-chain checks to continuous on-chain verification is becoming a non-negotiable regulatory requirement for tokenized funds.

This architectural change is critical for institutional adoption. As noted by industry analyses, regulated cross-chain bridges with embedded KYC checks now allow tokenized bonds issued on permissioned bank chains to be posted as collateral on public DeFi protocols. This interoperability relies on the certainty that the underlying identity data is current, immutable, and machine-readable. Without onchain KYC 2026, tokenized assets remain isolated from the broader financial system due to unresolved compliance risks.

The technology behind this shift includes verifiable credentials and zero-knowledge proofs, which allow investors to prove compliance while preserving data privacy. This balance of privacy and transparency is what distinguishes modern onchain KYC from legacy systems. As the market matures, the ability to programmatically enforce compliance will be the primary differentiator between viable tokenized products and those that fail regulatory scrutiny.

How AI identity verification works on chain

Onchain KYC 2026 represents a structural shift in regulatory compliance, moving identity verification from isolated databases to transparent, programmable logic. The core mechanism relies on AI to analyze unstructured identity data—such as government-issued documents and biometric scans—against global sanctions lists and adverse media. This analysis occurs off-chain to preserve privacy, but the result is a cryptographically signed attestation that lives on the blockchain.

AI models process these documents to extract key fields and verify authenticity, detecting forgeries or deepfakes that traditional optical character recognition (OCR) might miss. Once the AI confirms the data matches the claimed identity, the system generates a zero-knowledge proof or a signed credential. This credential serves as the bridge between the user’s private identity and the public ledger, ensuring that compliance is verifiable without revealing sensitive personal information.

Oracles play a critical role in this ecosystem by fetching real-time regulatory data and delivering the AI’s verification results to smart contracts. According to Chainlink, onchain KYC uses smart contracts and oracles to ensure that identity status is current and accurate at the moment of transaction. This allows tokenized asset platforms to automatically enforce compliance rules, such as restricting access to accredited investors or blocking sanctioned entities, without manual intervention.

Blockpass illustrates this approach through its On-Chain KYC® 2.0 framework, which allows issuers to create verifiable and reusable digital identities. Instead of re-verifying users for every new token sale, the smart contract checks the existing attestation. This reduces friction for compliant participants while maintaining a rigorous audit trail for regulators. The result is a compliance standard that is both scalable and immutable, aligning with the growing demand for transparent tokenized asset markets.

Leading onchain KYC solutions for 2026

The landscape of onchain KYC 2026 is defined by a shift from centralized databases to verifiable, decentralized identity protocols. As regulatory scrutiny intensifies, institutions are adopting platforms that integrate directly with smart contracts and oracles. The following analysis compares three primary approaches: Chainlink’s oracle-based infrastructure, Blockpass’s decentralized identity issuance, and KYC-Chain’s comprehensive compliance automation.

Chainlink ACE and DECO

Chainlink addresses the data connectivity gap by using decentralized oracles to bring off-chain identity attestations on-chain. Its ACE (Attestation, Compliance, and Encryption) framework allows verifiers to submit encrypted credentials that smart contracts can validate without exposing raw personal data. DECO extends this capability by enabling zero-knowledge proofs, ensuring that only necessary compliance data is shared. This architecture is critical for institutions requiring strict data minimization while maintaining full regulatory adherence.

Blockpass

Blockpass focuses on the issuance and management of decentralized identity credentials. Its On-Chain KYC 2.0 protocol enables issuers to create verifiable, reusable digital identities that function both on and off the blockchain. By leveraging self-sovereign identity principles, Blockpass allows users to hold their own compliance data in digital wallets. This reduces the burden on issuers to store sensitive information while providing a seamless verification experience for tokenized asset platforms.

KYC-Chain

KYC-Chain offers a centralized compliance layer that automates KYC, KYB, and AML screening through APIs and smart contract integrations. It provides real-time sanctions, PEP, and adverse media checks, making it suitable for platforms that require immediate, high-throughput verification. While less decentralized in its core architecture, KYC-Chain’s robust API infrastructure allows it to bridge traditional compliance workflows with onchain applications efficiently.

| Provider | Identity Model | Supported Chains | Integration Method |

|---|---|---|---|

| Chainlink ACE/DECO | Oracle-based Attestations | Multi-chain (EVM, Solana, etc.) | Smart Contract Oracles |

| Blockpass | Decentralized Identity (SSI) | Multi-chain (EVM, Polygon, etc.) | Wallet SDK & API |

| KYC-Chain | Centralized Compliance Layer | Multi-chain (EVM, Cosmos, etc.) | API, iFrame, White-label |

Implementing Real-Time Onchain KYC Solutions

Integrating onchain KYC 2026 into existing infrastructure requires a structured approach that bridges traditional compliance mandates with decentralized technology. For developers and compliance officers, the goal is to embed verification directly into the smart contract layer, ensuring that only verified identities can interact with tokenized assets. This process relies on privacy-preserving attestations and oracle networks to validate user status without revealing sensitive personal data on public ledgers.

The following steps outline the critical workflow for deploying these systems securely and in accordance with current regulatory standards.

Begin by mapping jurisdictional AML (Anti-Money Laundering) and KYC obligations to specific smart contract functions. Identify which user actions—such as token transfers, staking, or collateral posting—trigger verification checks. This audit ensures that the technical architecture aligns with legal mandates before any code is written.

Choose a provider that supports zero-knowledge proofs or similar cryptographic methods. Solutions like Blockpass or emerging on-chain KYC 2.0 platforms allow users to generate reusable digital identities. This step is critical for maintaining user privacy while providing the necessary attestations to smart contracts.

Connect your smart contracts to reliable oracle services, such as Chainlink, to fetch real-time verification status. Oracles act as the bridge between off-chain identity providers and on-chain logic, ensuring that the contract can dynamically check if a user holds a valid KYC attestation before allowing transactions.

Rigorously test the integration using sandbox environments that simulate various user states (verified, unverified, expired). Ensure that the system correctly blocks non-compliant addresses and accepts valid ones. This phase validates that the real-time checks function as intended under load and edge cases.

Launch the solution on the mainnet with continuous monitoring tools. Regularly audit the oracle feeds and attestation validity periods to ensure ongoing regulatory compliance. This final step ensures that the onchain KYC 2026 framework remains robust against evolving regulatory landscapes.

By following this structured implementation path, organizations can achieve seamless regulatory compliance while preserving the efficiency and transparency inherent in blockchain technology. The integration of real-time verification transforms onchain KYC 2026 from a theoretical concept into a practical, enforceable standard for the future of digital finance.

Frequently asked questions about onchain KYC

How does onchain KYC 2026 differ from traditional off-chain verification?

Traditional off-chain KYC relies on static databases that are prone to data decay and do not automatically update when an investor’s status changes. Onchain KYC 2026 embeds verification into smart contracts using oracles and zero-knowledge proofs, enabling continuous, real-time compliance checks that trigger automatically during asset transfers.

Can tokenized assets be transferred without a valid KYC attestation?

No. In regulated environments, smart contracts are programmed to reject transactions from addresses that lack a valid, current attestation. This ensures that only verified participants can interact with the asset, preventing compliance violations such as transfers to sanctioned entities or non-accredited investors.

How is user privacy maintained during on-chain verification?

Onchain KYC utilizes zero-knowledge proofs (ZKPs) and verifiable credentials to allow users to prove compliance without revealing underlying personal data on the public ledger. This ensures that regulatory requirements are met while adhering to data minimization principles and privacy standards.

No comments yet. Be the first to share your thoughts!