What onchain KYC 2026 actually means

Onchain KYC 2026 is not a static database of passport scans. It is a dynamic, privacy-preserving protocol that uses zero-knowledge proofs (ZKPs) to verify identity without exposing raw personal data. Instead of uploading sensitive documents to a centralized server, users generate cryptographic proofs that confirm they meet specific criteria—such as being over 18 or residing in a permitted jurisdiction—without revealing who they are.

This shift transforms compliance from a data-hoarding exercise into a verification service. Traditional KYC relies on sharing copies of IDs with every new platform, creating massive honeypots for hackers. Onchain KYC 2026 flips this model. Users hold their verified credentials in a digital wallet and present only the necessary proof to smart contracts. This approach aligns with emerging regulatory expectations for data minimization while maintaining the auditability required by financial authorities.

The infrastructure relies on oracles and verifiable credentials to bridge off-chain identity providers with on-chain smart contracts. Services like Blockpass and Chainlink are already building the attestations that make this possible. By decoupling identity verification from data storage, DeFi protocols can comply with Anti-Money Laundering (AML) standards without compromising user privacy or security.

Zero-knowledge proofs for privacy

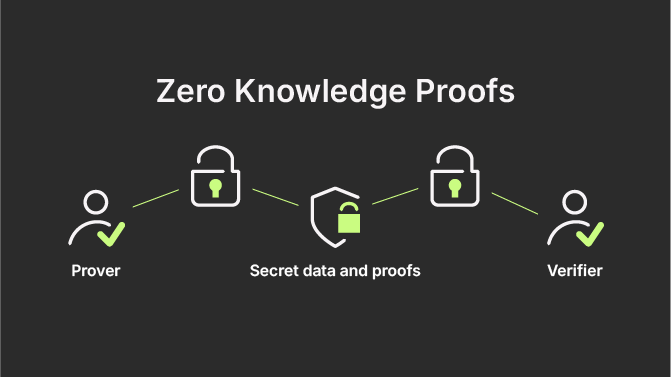

Traditional onchain KYC often feels like handing your passport to a stranger to prove you are over 21. Zero-knowledge proofs (ZKPs) change this dynamic entirely. They allow a user to generate a cryptographic proof that they meet specific criteria—such as being over 18, not residing in a sanctioned jurisdiction, or holding a valid government ID—without revealing the underlying data.

In this system, the user’s identity documents are verified by a trusted oracle or attester off-chain. Once verified, the oracle issues a ZK-proof. This proof is a mathematical guarantee that can be submitted to a smart contract. The contract validates the proof instantly and emits a simple binary signal: true or false. The contract never sees the user’s name, address, or passport number.

This mechanism is the technical backbone of privacy-preserving onchain KYC 2026. It decouples compliance from data exposure. Financial institutions can enforce Anti-Money Laundering (AML) rules while users retain control over their personal information. The proof acts as a digital seal of approval, verifying eligibility without compromising identity.

The architecture typically involves three parties: the user, the verifier (oracle), and the smart contract. The user interacts with the verifier to generate the proof. The verifier checks the user’s credentials against regulatory databases. If the credentials are valid, the verifier signs the proof. The user then submits this signed proof to the smart contract, which executes the appropriate action based on the result.

This approach solves the fundamental tension in DeFi compliance: the need for regulatory oversight versus the desire for financial privacy. By using ZKPs, platforms can onboard institutional capital without forcing users to surrender their anonymity. The proof is the bridge between the regulated world and the decentralized one.

Leading onchain KYC 2026 providers

The onchain KYC 2026 landscape is defined by a shift from centralized data hoarding to decentralized, privacy-preserving attestations. Providers now compete on how efficiently they can verify identity without exposing raw personal data, leveraging zero-knowledge proofs and selective disclosure models. This approach allows users to prove compliance—such as being over 18 or passing an AML check—without revealing their name, address, or full transaction history.

Blockpass

Blockpass operates as a foundational infrastructure layer for digital identity, enabling organizations to issue verifiable credentials that are stored on-chain. Their On-Chain KYC® 2.0 model focuses on reusability, allowing users to hold their verified status in a digital wallet and present it to multiple DeFi protocols or institutions without repeating the verification process. This reduces friction for users and lowers compliance costs for providers by creating a single source of truth for identity status.

Togggle

Togggle emphasizes a streamlined user experience by integrating KYC verification directly into the flow of decentralized applications. Their solution prioritizes efficiency and privacy, using cryptographic methods to ensure that only the necessary attestation data is shared with the requesting protocol. By abstracting the complexity of blockchain identity, Togggle aims to make compliance invisible to the end-user while maintaining strict adherence to regulatory standards.

Comparison of Provider Models

The following table compares the core technical approaches of leading providers in the onchain KYC 2026 space, highlighting differences in privacy architecture and blockchain compatibility.

| Provider | Privacy Model | Supported Chains | Attestation Type |

|---|---|---|---|

| Blockpass | Zero-Knowledge Proofs | Multi-chain (EVM, Solana) | Reusable Verifiable Credentials |

| Togggle | Selective Disclosure | EVM-focused | Real-time Verification Tokens |

| Spruce ID | Decentralized Identifiers (DIDs) | Multi-chain | W3C Standard Credentials |

| Polygon ID | Zero-Knowledge Circuits | Polygon zkEVM | ZK-Attestations |

Real-world DeFi compliance applications

Onchain KYC 2026 is no longer theoretical. Institutional players are actively deploying zero-knowledge proofs to satisfy regulatory requirements without exposing sensitive personal data. This shift allows financial products to operate on public blockchains while maintaining strict adherence to anti-money laundering (AML) and counter-terrorism financing (CFT) standards.

Tokenized Money Market Funds

Tokenized funds represent one of the most immediate use cases for verified onchain identity. In this model, fund shares exist as permissioned tokens on a public blockchain. The issuer retains control over who can hold these tokens, but the verification process is automated. Instead of manual reviews, smart contracts check for valid cryptographic proofs of identity before allowing transfers or dividends.

This approach streamlines the investor onboarding process. For example, Eco’s support documentation outlines how tokenized money market funds can be held onchain, emphasizing that the issuer’s compliance layer handles the heavy lifting. Investors benefit from the liquidity and transparency of public chains, while institutions retain the ability to enforce eligibility criteria. The result is a product that feels like a traditional mutual fund but settles like a cryptocurrency.

Cross-Chain Collateral Bridges

Cross-chain bridges face intense scrutiny due to their role in moving value between isolated networks. A regulated bridge with embedded KYC checks can allow a tokenized bond issued on a permissioned bank chain to be posted as collateral on a public DeFi protocol. This requires the bridge to verify that the user holds a valid identity credential without revealing their underlying bank account details.

By integrating onchain KYC 2026 standards into these bridges, financial institutions can unlock trillions in dormant traditional finance assets. The bridge acts as a compliance gatekeeper, ensuring that only verified entities can interact with the liquidity pools. This maintains regulatory adherence while preserving the composability and liquidity that define the DeFi ecosystem.

Web3 regulatory compliance checklist

Integrating onchain KYC 2026 requires balancing AML/CFT mandates with zero-knowledge privacy. Projects must verify identity without storing raw personal data on-chain, relying instead on cryptographic attestations. This checklist outlines the critical steps for compliance.

Choose a provider that issues verifiable credentials using zero-knowledge proofs. Ensure the provider supports standard protocols like W3C Verifiable Credentials to maintain interoperability across DeFi protocols.

Determine which specific regulatory checks your users must pass, such as FATF Travel Rule compliance or sanctions screening. Map these requirements to specific ZK-proof attributes so users only reveal what is necessary for compliance.

Connect your smart contracts to oracle networks that fetch real-time compliance data. Oracles act as bridges, validating on-chain attestations against off-chain regulatory databases without exposing user identity details.

Deploy testnet environments to simulate user flows. Verify that the smart contract correctly rejects non-compliant wallets and accepts valid ZK-proofs, ensuring no false positives block legitimate users.

No comments yet. Be the first to share your thoughts!