What on-chain KYC actually means

On-chain KYC is the process of verifying user identity for blockchain applications using smart contracts and oracles. It represents a structural shift from traditional off-chain verification, where users submit documents to centralized platforms, toward a model where identity is verified cryptographically and managed through decentralized protocols.

The core mechanism relies on cryptographic proofs rather than raw data sharing. Instead of storing personal information like passports or social security numbers directly on the blockchain—which would violate privacy regulations—systems store verifiable attestations. These attestations are digital credentials that confirm a user meets specific criteria, such as being a real person or passing an anti-money laundering (AML) check, without revealing the underlying personal details.

This approach enables institutions to meet regulatory standards while preserving user privacy. Smart contracts can automatically check these proofs before allowing access to financial services, creating a seamless compliance layer that operates without the friction of manual document review. The technology links real-world identity attributes or digital reputation to a blockchain address, ensuring that the entity interacting with the protocol is who they claim to be.

The Shift to Automated Compliance

The 2026 landscape is defined by the transition from reactive, manual compliance to automated, on-chain enforcement. Traditional KYC processes are often siloed, requiring users to re-verify their identity for every new platform. On-chain KYC solves this by creating portable identity credentials that can be reused across different applications.

This automation reduces the risk of human error and speeds up onboarding times from days to seconds. By integrating compliance directly into the code of smart contracts, platforms can ensure that only verified users interact with their services. This creates a more secure environment for institutional investors and retail users alike, as the identity of every participant is cryptographically guaranteed.

The shift also addresses the growing complexity of cross-border transactions. With on-chain KYC, compliance checks can be performed in real-time against global regulatory databases, ensuring that transactions adhere to local laws without requiring intermediaries. This level of automation is essential for the mainstream adoption of blockchain technology, as it bridges the gap between decentralized innovation and regulatory oversight.

Why It Matters for 2026

As regulatory scrutiny increases, the ability to prove identity on-chain becomes a competitive advantage. Platforms that adopt on-chain KYC can offer faster, more secure services while maintaining strict compliance with global standards. This is particularly important for decentralized finance (DeFi) protocols, which have historically struggled with regulatory uncertainty.

By embedding compliance into the architecture of blockchain applications, developers can create products that are both innovative and legally sound. This approach not only protects users from fraud and identity theft but also builds trust with regulators and institutional partners. The result is a more resilient and sustainable ecosystem for blockchain technology.

The move toward automated compliance is not just a technical upgrade; it is a fundamental change in how identity and trust are managed in the digital age. As more platforms adopt these standards, on-chain KYC will become the norm rather than the exception, shaping the future of digital finance.

Why 2026 marks a compliance turning point

The landscape of digital asset regulation has shifted from theoretical frameworks to immediate, enforceable mandates. In 2026, the pressure on crypto-native businesses is no longer about future-proofing; it is about survival under current laws. The convergence of the European Union’s Markets in Crypto-Assets (MiCA) regulation and the Financial Action Task Force (FATF) Travel Rule creates a unified global standard that legacy systems cannot meet.

Manual compliance processes, once sufficient for small-scale exchanges, are now operational liabilities. MiCA requires institutions to perform continuous transaction monitoring and identity verification at scale. Simultaneously, the FATF Travel Rule mandates that virtual asset service providers share originator and beneficiary information for transactions exceeding specific thresholds. Attempting to handle these requirements through spreadsheets, email chains, or isolated databases introduces unacceptable latency and error rates.

Automated on-chain compliance is no longer a competitive advantage—it is the baseline for market entry. By embedding regulatory checks directly into smart contracts and token standards, platforms can enforce investor eligibility, transfer restrictions, and reporting obligations in real time. This approach reduces operational overhead while ensuring that compliance is not an afterthought, but a core feature of the financial infrastructure.

How automated AML checks work on-chain

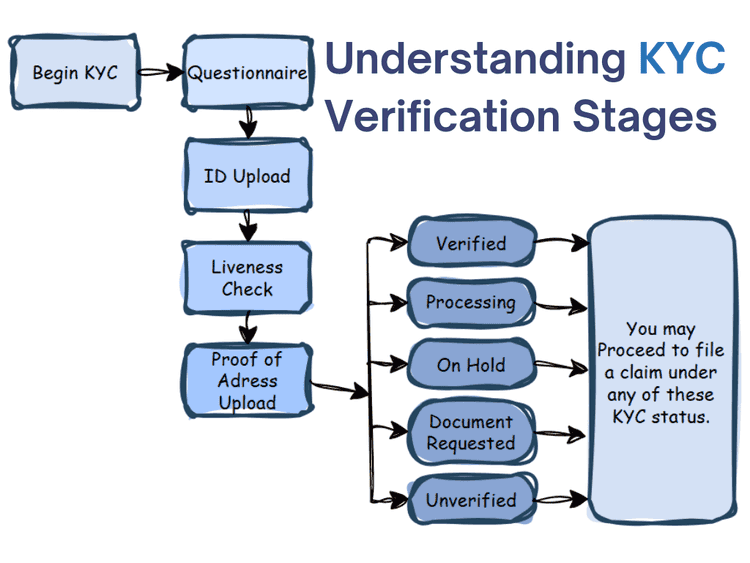

Automated on-chain KYC replaces manual, reactive reviews with real-time, programmatic enforcement. The system functions as a continuous loop: oracles fetch identity attestations, smart contracts evaluate transaction risk against regulatory rules, and zero-knowledge proofs verify compliance without exposing sensitive personal data. This architecture allows institutions to meet Anti-Money Laundering (AML) standards while preserving the privacy essential to decentralized finance.

The process begins with identity verification. Users submit credentials to an off-chain identity provider. Once validated, the provider generates a cryptographic attestation—a digital signature proving the user’s status (e.g., "accredited investor" or "sanction-free")—which is stored on-chain or in a decentralized identity registry. This attestation is not raw personal data; it is a reusable, privacy-preserving token that can be presented to various protocols without re-verifying the user’s identity from scratch.

Oracles fetch real-world data

Smart contracts cannot natively access off-chain data, such as global sanctions lists or credit scores. Oracles bridge this gap by fetching and verifying this information from trusted external sources. Chainlink, for example, provides decentralized oracle networks that deliver real-time data feeds to smart contracts. These oracles ensure that the data used for compliance checks is accurate, tamper-proof, and updated frequently, allowing protocols to react to changing regulatory landscapes instantly.

Smart contracts evaluate risk scores

Once an oracle delivers the necessary data, the smart contract executes the compliance logic. The contract checks the user’s on-chain transaction history against predefined risk parameters. For instance, if a wallet interacts with a known darknet market or a sanctioned entity, the contract flags the transaction. The risk score is calculated in real-time, determining whether the transaction proceeds, requires additional verification, or is blocked entirely. This automated evaluation ensures consistent application of AML policies across all users and transactions.

Zero-knowledge proofs preserve privacy

A core challenge in on-chain compliance is balancing transparency with privacy. Zero-knowledge proofs (ZKPs) solve this by allowing a user to prove they meet certain criteria without revealing the underlying data. For example, a user can prove they are not on a sanctions list without disclosing their name, address, or transaction history. This cryptographic technique ensures that regulatory compliance does not come at the cost of personal privacy, a critical feature for maintaining user trust in decentralized systems.

The result is a seamless integration of regulatory compliance into the blockchain’s core infrastructure. By automating AML checks through oracles, smart contracts, and ZKPs, protocols can operate legally and securely without compromising the decentralized nature of the technology. This shift represents a fundamental change in how digital assets are governed, moving from post-hoc investigations to proactive, automated prevention.

Privacy-preserving verification models

On-chain KYC shifts the compliance burden from centralized databases to cryptographic proofs. Instead of uploading a passport scan to a server, users generate zero-knowledge proofs that confirm they meet regulatory thresholds without revealing the underlying personal data.

This approach allows institutions to satisfy Anti-Money Laundering (AML) and Counter-Terrorist Financing (CFT) standards while keeping sensitive identity details private. The verification process relies on smart contracts and oracles to validate attestations, ensuring that compliance is programmable and auditable without exposing raw user information.

| Verification Model | Data Storage | User Privacy | Automation Level |

|---|---|---|---|

| Traditional KYC | Centralized Database | Low (Raw data exposure) | Low (Manual review) |

| On-Chain KYC | Decentralized Attestations | High (Zero-knowledge proofs) | High (Smart contract execution) |

Traditional KYC requires users to share unencrypted documents with service providers, creating a single point of failure for data breaches. In contrast, on-chain models store only the cryptographic proof of compliance on the blockchain. The actual identity documents remain off-chain or are hashed, meaning the service provider never sees the user's face or government ID number.

Services like Blockpass On-Chain KYC enable corporate customers to issue verifiable digital identities. These attestations can be reused across multiple platforms, reducing friction for users who need to prove their status to different exchanges or DeFi protocols. The system empowers users to control their data, sharing only the minimum necessary proof to access services.

Implementing on-chain compliance workflows

Moving from concept to production requires treating identity verification as a core infrastructure component rather than an afterthought. Platforms must bridge the gap between traditional regulatory requirements and decentralized identity standards. The goal is to automate the heavy lifting of sanctions screening and risk scoring while keeping the user experience frictionless.

1. Select the integration method

Most providers like KYC-Chain offer API endpoints, iFrames, or white-label solutions. APIs give engineering teams full control over the data flow and UI customization, which is essential for complex platforms. iFrames are faster to deploy but offer less control over the user journey. Choose the method that aligns with your technical capacity and brand requirements.

2. Design the user journey

The verification process should feel like a single step, not a bureaucratic hurdle. Use progressive disclosure to ask for only the necessary information at each stage. If a user is already verified by a trusted partner, allow them to skip redundant steps using existing credentials. The interface must clearly explain why data is being collected to maintain trust.

3. Implement real-time monitoring

Static verification is insufficient for ongoing compliance. Integrate continuous monitoring tools that scan for adverse media, political exposure, or changes in sanctions lists. These tools should trigger alerts or lock accounts automatically when risk thresholds are exceeded. This reduces the manual workload for compliance teams and ensures immediate reaction to emerging threats.

4. Handle edge cases gracefully

Not every user will pass verification on the first attempt. Build robust error handling for failed ID scans, blurred photos, or mismatched facial recognition. Provide clear, actionable feedback so users can retry without frustration. For high-risk cases, route users to a manual review queue with all relevant data pre-loaded for the compliance officer.

Review existing APIs and data storage to ensure they can handle sensitive identity data securely. Identify gaps in your current KYC/AML coverage.

Evaluate providers like KYC-Chain or On-ChainPass based on their API reliability, global coverage, and compliance certifications.

Connect the provider’s API to your platform’s backend. Implement webhooks for real-time status updates and ensure data encryption in transit.

Run beta tests with a small group of users to identify friction points in the verification process. Gather feedback on clarity and speed.

Roll out the feature to all users. Continuously monitor success rates and false positives to refine your risk models.

Common questions about on-chain identity

On-chain identity verification is evolving from manual reviews to automated, privacy-preserving protocols. Below are answers to frequent questions about how these systems work and how to monitor them.

No comments yet. Be the first to share your thoughts!