What is onchain KYC?

Onchain KYC is the process of verifying user identity for blockchain applications using smart contracts and oracles. It enables institutions to meet regulatory standards like AML/CFT while preserving user privacy through cryptographic proofs rather than raw data sharing.

Think of it as a digital ID card that proves you are who you say you are without showing your entire life history. Instead of uploading your passport to a central database, you generate a zero-knowledge proof. This proof confirms you are over 18 or not on a sanctions list without revealing your name, address, or birthdate.

The system relies on decentralized identity protocols to issue these verifiable credentials. Once verified, the data stays on your device or in a secure vault. You only share the specific proof required for a transaction, keeping your personal information private.

How do I verify my onchain wallet?

Verification methods vary by platform, but the process generally follows a similar path. You typically need to link a centralized account to your wallet to initiate the check.

- Sign in to a compliant platform: Most users start by logging into a service like Coinbase or a dedicated identity provider.

- Complete the verification flow: Access the KYC section and submit required documents for review.

- Claim your onchain attestation: Once approved, you connect your wallet to receive a verifiable credential or badge.

This process creates a reusable digital identity. You can use the same verification across multiple DeFi protocols without repeating the submission process.

Does crypto wallet need KYC?

Not all wallets require identity checks. Non-custodial wallets, such as MetaMask or Trust Wallet, allow you to create an account and hold assets without any personal information. These are often called "no KYC" wallets.

However, there are limits. While the wallet itself may not ask for ID, interacting with regulated services often does. If you want to move funds to a centralized exchange or use a fiat on-ramp, you will likely face compliance checks. Additionally, some jurisdictions may require identification for certain types of transactions or high-value transfers.

Always check the specific policy of the wallet and the services you plan to use. Privacy is preserved onchain, but regulatory compliance often requires it offchain.

Onchain KYC choices that change the plan

Implementing onchain KYC is not a binary choice between compliance and anonymity. It is a series of engineering and legal decisions that determine who holds your data, how it is verified, and what happens when regulations change. Before integrating any solution, you must evaluate the specific friction points each model introduces to the user journey.

Centralized vs. decentralized verification

Centralized providers offer a streamlined user experience but create single points of failure. If the provider suffers an outage or changes its API terms, your application’s onboarding process breaks immediately. You also store or transmit sensitive PII to a third party, increasing your liability under GDPR or CCPA. Decentralized attestations shift this risk. Users hold their own credentials, and smart contracts verify status without you ever seeing the raw identity data. This reduces your compliance burden but requires users to manage multiple wallets or attestations, which can increase drop-off rates during onboarding.

Privacy preservation vs. regulatory scrutiny

Zero-knowledge proofs (ZKPs) allow you to verify that a user meets specific criteria—such as being over 18 or not on a sanctions list—without revealing their name or address. This is the gold standard for privacy. However, regulators are still adapting to this technology. Some jurisdictions may reject ZK-based KYC if they cannot audit the underlying identity source directly. You must decide if your target market prioritizes user privacy (favoring ZKPs) or regulatory ease (favoring traditional document verification). The tradeoff is clear: ZKPs protect user data but may face slower regulatory adoption, while traditional methods are widely accepted but expose more personal information.

Cost structure and scalability

The cost of onchain KYC varies significantly based on the verification method. Traditional document verification involves manual or semi-automated review, which can cost $2–$5 per user and introduce latency. Onchain attestation models often have lower marginal costs once the infrastructure is built, but you may pay for oracle services or gas fees for each verification check. For high-volume DeFi applications, even small per-transaction costs can add up. Evaluate whether your user base justifies the upfront development cost of a ZK-proof system or if a simpler, API-based check from a provider is more appropriate for early-stage growth.

| Factor | Centralized | Decentralized |

|---|---|---|

| Data Control | Provider holds PII | User holds credentials |

| Compliance Risk | Shared liability | Lower direct liability |

| User Friction | Lower (single sign-on) | Higher (wallet management) |

| Privacy | Minimal | High (ZK-proofs) |

How to Choose an Onchain KYC Provider

Selecting the right identity infrastructure requires balancing regulatory compliance, user privacy, and technical integration. Onchain KYC is the process of verifying user identity for blockchain applications using smart contracts and oracles. It enables institutions to meet regulatory standards (like AML/CFT) while preserving user privacy through cryptographic proofs rather than raw data sharing.

However, not all solutions are created equal. Some providers focus on reusable attestations for broad DeFi use, while others offer specialized verification for specific jurisdictions or exchange withdrawals. The following framework helps you evaluate providers based on four critical dimensions.

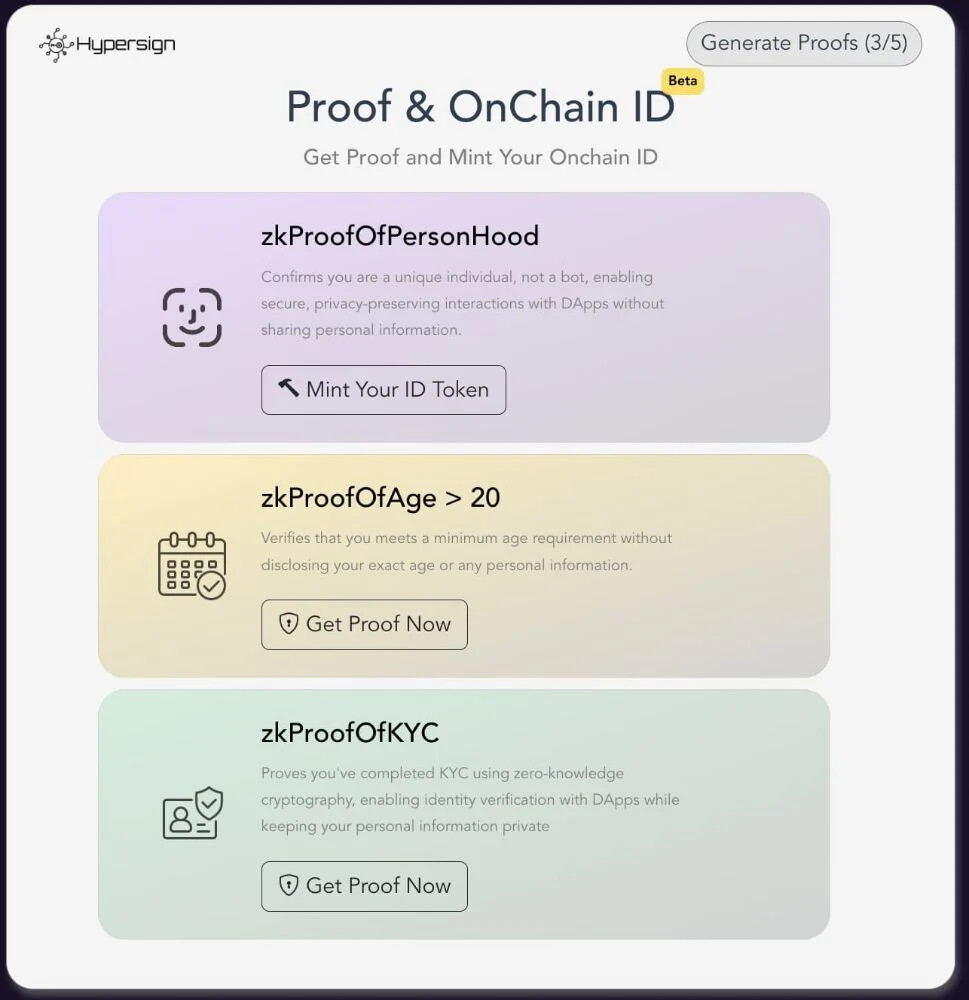

Prioritize providers that use zero-knowledge proofs (ZKPs) or similar cryptographic methods. The goal is to verify that a user is compliant without exposing who they are. Avoid platforms that store raw PII (Personally Identifiable Information) on-chain or in accessible databases. Look for explicit statements about "data minimization" and "privacy-by-design" in their technical documentation.

Ensure the provider supports reusable digital identity attestations. This allows users to verify their identity once and use that credential across multiple DeFi protocols or institutions without repeating the process. Standards like Blockpass’s On-Chain KYC 2.0 empower issuers to create verifiable, reusable credentials that work on and off the blockchain, reducing friction for both users and integrators.

KYC requirements vary significantly by region. A provider that is compliant in the EU may not satisfy US or Asian regulatory bodies. Check if the provider supports the specific jurisdictions your user base resides in. Some "no KYC" wallets still require compliance for certain jurisdictions or exchange withdrawals, so ensure your chosen provider aligns with your target market’s legal obligations.

Look for providers that offer clean SDKs or API documentation for seamless integration into your smart contracts or front-end. The best onchain KYC solutions should feel invisible to the user. If the verification process requires users to sign multiple transactions or navigate complex interfaces, adoption will suffer. Test the developer experience before committing to a long-term partnership.

Spotting Weak OnChain KYC Options

OnChain KYC promises privacy through zero-knowledge proofs, but the market is crowded with misleading claims. Many platforms advertise "non-custodial" identity solutions that still leak metadata or require centralized attesters. Before integrating a solution or verifying your wallet, check for these common pitfalls.

Vague "Zero-Knowledge" Claims

Not all ZK-proofs are created equal. Some providers use weak cryptographic parameters or rely on trusted setups that can be compromised. Look for proofs that have been audited by independent security firms. If the documentation doesn't specify the proof system (e.g., zk-SNARKs vs. zk-STARKs) or the verification key size, treat it as a red flag.

Centralized Verifiers in Disguise

A true decentralized KYC system should not rely on a single entity to issue or revoke attestations. If a platform requires you to upload a passport to a specific company's server, it's not on-chain identity—it's just a database. Check if the attestation is signed by a distributed set of verifiers or a DAO. The Blockpass model, for instance, allows multiple issuers, reducing single points of failure.

Lack of Standardization

Many solutions use proprietary data formats that don't interoperate with other DeFi protocols. This forces users to re-verify for every new platform, defeating the purpose of reusable identity. Look for adherence to W3C Verifiable Credentials or similar open standards. Without interoperability, your KYC status is trapped in a walled garden.

Hidden Data Retention

Even if the proof is on-chain, the underlying data might be stored off-chain by the issuer. If the issuer goes offline or sells the data, your privacy is gone. Check the data retention policy. The best solutions ensure that no raw personal data is ever stored in a way that can be linked back to your wallet address without your explicit consent.

Onchain KYC: what to check next

Addressing practical objections helps clarify how onchain identity verification fits into your workflow. These answers cover the core mechanics, verification steps, and regulatory realities you need to know before committing funds.

No comments yet. Be the first to share your thoughts!